Base offers DeFi lending yields ranging from 3-8% APY on stablecoins through protocols like Aave and Morpho, with transaction costs under $0.01. As Coinbase's Layer 2 network, Base combines institutional-grade infrastructure with the permissionless nature of DeFi, making it an attractive destination for yield-seeking lenders.

This guide covers everything you need to know about earning yield through lending on Base. From current market rates to protocol comparisons and step-by-step instructions, you will learn how to maximize returns while managing risk on this growing network.

Why Base for DeFi Lending?

Base has emerged as one of the most compelling Layer 2 networks for DeFi lending. Several factors contribute to its appeal for both new and experienced DeFi users.

Ultra-Low Transaction Costs

Gas fees on Base typically cost less than $0.01 per transaction. Compare this to Ethereum mainnet, where a simple lending transaction can cost $5-50 depending on network congestion. These savings compound quickly for active DeFi users who deposit, withdraw, and rebalance positions regularly.

For smaller depositors, low fees make DeFi lending economically viable. A user depositing $500 worth of USDC can actually earn meaningful yield without transaction costs eating into returns.

Coinbase Backing and Security

Base is built on the OP Stack and incubated by Coinbase, one of the most regulated and well-capitalized companies in crypto. This institutional backing provides several advantages:

- Strong developer resources and ecosystem support

- Institutional-grade infrastructure and security practices

- Clear regulatory positioning

- Access to Coinbase's user base of over 100 million verified users

The network inherits Ethereum's security through its rollup architecture while benefiting from Coinbase's operational expertise.

Growing DeFi Ecosystem

Base has attracted major DeFi protocols and significant total value locked (TVL). The network hosts Aave, Morpho, Compound, and numerous other lending platforms. This competition benefits users through better rates and more options.

Liquidity depth continues to grow as more capital flows into Base DeFi. Deeper liquidity means better execution, tighter spreads, and more stable yields over time.

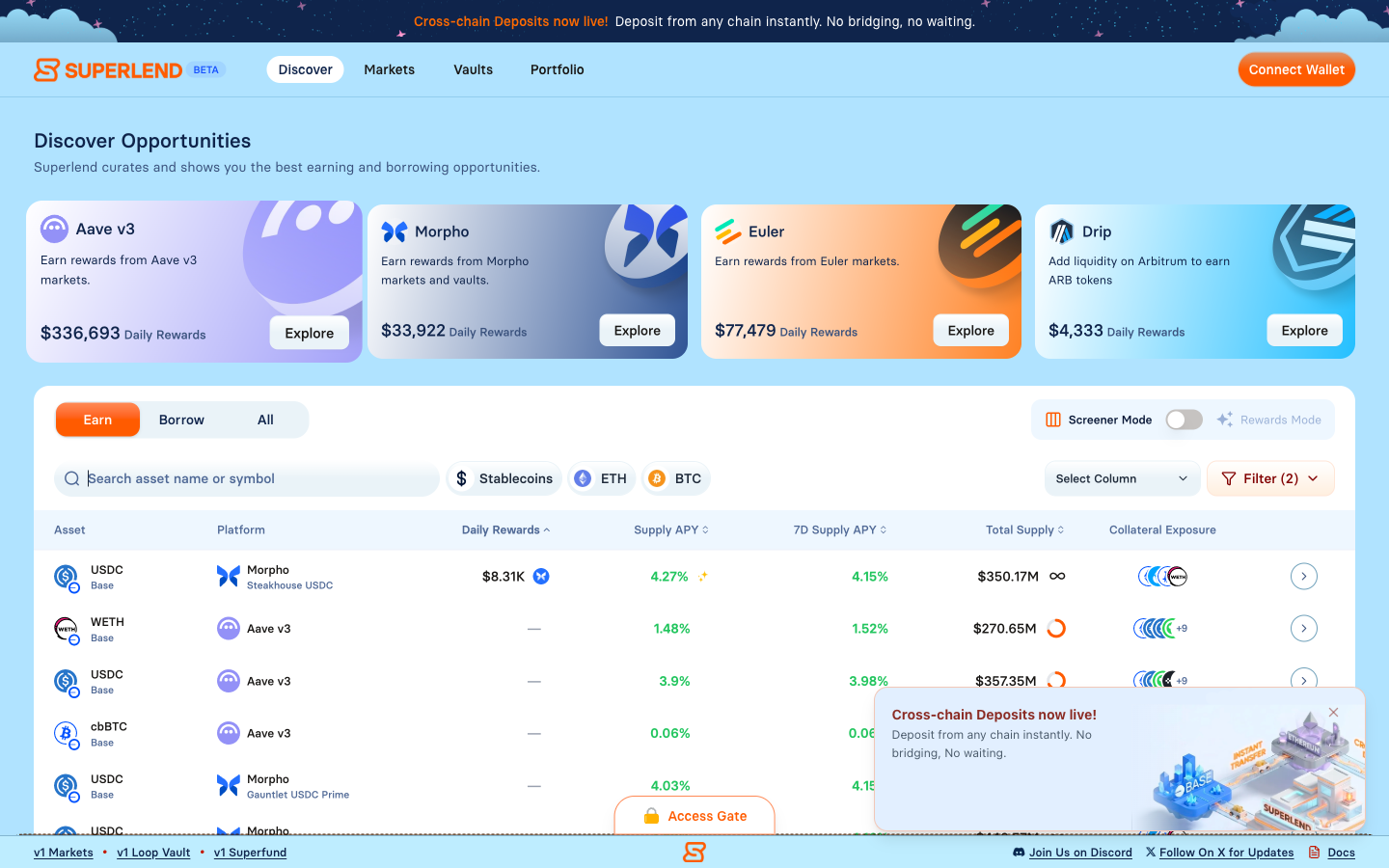

DeFi lending markets on Base chain, aggregated through Superlend.

DeFi lending markets on Base chain, aggregated through Superlend.

Current Base Lending Rates

Lending rates on Base vary by asset and protocol. Understanding the current yield landscape helps you make informed decisions about where to deploy capital.

Stablecoin Yields

USDC lending on Base currently offers the most opportunities:

- Aave v3: USDC supply rates range from 3.5-4.5% APY depending on utilization

- Morpho Vaults: Optimized USDC vaults offer 4-4.5% APY with active management

- Compound v3: USDC rates typically fall in the 3-4% APY range

USDT and DAI are also available on some platforms, though with lower liquidity than USDC.

ETH and WETH

Ethereum-denominated assets earn lower base yields but offer exposure to ETH price appreciation:

- Native ETH/WETH supply rates: 1.5-3% APY across protocols

- Some protocols offer additional incentives that boost effective yields

Other Assets

Base supports lending of various assets including:

- cbETH (Coinbase staked ETH)

- wstETH (Lido staked ETH)

- Various governance tokens

Yields on these assets fluctuate based on borrowing demand and protocol incentives.

Protocols on Base

Several major lending protocols operate on Base, each with distinct characteristics and yield profiles.

Aave v3

Aave represents the most battle-tested lending protocol on Base. Key features include:

- Isolation mode for newer assets

- Efficiency mode (E-Mode) for correlated asset pairs

- Proven smart contract security with years of mainnet operation

- Deep liquidity across major assets

Aave's Base deployment mirrors its Ethereum mainnet functionality, giving users a familiar experience with lower costs. The protocol supports both variable and stable rate borrowing, though most users stick with variable rates.

For a deeper understanding of how Aave and similar protocols work, read our complete guide to DeFi lending.

Morpho

Morpho takes a different approach to lending optimization. The protocol operates through curated vaults managed by risk experts:

- Vaults allocate deposits across multiple markets for optimized yields

- Risk curators manage exposure and rebalancing

- Users can choose vaults matching their risk preferences

- Higher yields through efficient capital allocation

Morpho vaults on Base have attracted significant deposits, particularly in USDC-denominated strategies. The vault structure simplifies yield farming while maintaining transparency about underlying allocations.

Explore available Morpho vaults on Base through Superlend's vault discovery.

Compound v3

Compound's third major iteration operates on Base with a streamlined design:

- Single-asset markets focused on major stablecoins

- Simplified user experience

- Strong security track record

- Active governance and protocol development

Other Protocols

Base hosts additional lending options including:

- Moonwell: Native to Base with competitive rates and governance incentives

- Seamless Protocol: Designed specifically for Base's ecosystem

- Various yield aggregators: Automated strategies that optimize across protocols

How to Lend on Base Through Superlend

Superlend functions as a non-custodial DeFi lending aggregator that simplifies access to Base lending opportunities. Rather than manually comparing rates across protocols, Superlend displays yields from multiple platforms in a unified interface.

Step 1: Connect Your Wallet

Navigate to Superlend's discover page and connect a compatible wallet. Superlend supports MetaMask, WalletConnect, Coinbase Wallet, and other major providers.

Ensure your wallet is connected to the Base network. Most wallets allow network switching directly from the interface.

Step 2: Bridge Assets to Base

If your assets are on Ethereum mainnet or another network, you will need to bridge them to Base. Options include:

- Coinbase: Direct withdrawals to Base for Coinbase users

- Official Base Bridge: Native bridge from Ethereum

- Third-party bridges: Stargate, Across, and others offer fast bridging

Consider bridge fees and time when calculating overall yield. Native Coinbase withdrawals to Base are typically free and instant for Coinbase users.

Step 3: Compare Yields

Superlend aggregates lending rates across Base protocols. The interface displays:

- Current APY for each asset on each protocol

- Historical rate trends

- TVL and liquidity metrics

- Protocol risk indicators

Sort by yield, TVL, or protocol to find opportunities matching your criteria. For stablecoin strategies, our USDC lending guide provides additional context on maximizing stablecoin yields.

Step 4: Deposit

Select your target protocol and asset. Superlend routes your transaction directly to the underlying protocol smart contracts. Your funds remain in the protocol's custody – Superlend never holds user assets.

Approve the token spend (first-time only) and confirm the deposit transaction. On Base, both transactions typically cost less than $0.02 combined.

Step 5: Monitor and Manage

Track your positions through Superlend's portfolio view. The dashboard shows:

- Current balances and earned interest

- Real-time APY for active positions

- Option to withdraw or rebalance

Yields fluctuate based on borrowing demand. Periodic review helps ensure your capital remains deployed in optimal positions.

Base vs Ethereum Mainnet

Understanding the tradeoffs between Base and Ethereum mainnet helps inform your network choice for DeFi lending.

Cost Comparison

On Ethereum mainnet, a token approval costs $3-15, deposits and withdrawals run $10-50 each, and position management transactions cost $5-30. On Base, the same actions cost a fraction of a cent: approvals at $0.001, deposits and withdrawals at $0.005, and position management at $0.003.

For a user making monthly deposits and quarterly rebalancing, annual gas costs might reach $200+ on mainnet versus under $1 on Base.

Yield Comparison

Mainnet and Base yields often differ due to varying liquidity and utilization:

- Mainnet typically offers slightly higher raw yields due to greater borrowing demand

- Base yields often outperform on a net basis after accounting for gas savings

- Incentive programs can temporarily boost Base yields above mainnet

Security Considerations

Both networks offer strong security, with different trust assumptions:

- Ethereum Mainnet: Direct Layer 1 security, no additional trust assumptions

- Base: Inherits Ethereum security through rollup, adds trust in sequencer

For most users, Base's security model provides adequate protection while enabling dramatically lower costs. Large depositors with significant capital might prefer mainnet's minimal trust assumptions despite higher costs.

Liquidity Depth

Mainnet maintains deeper liquidity for most assets. This matters for:

- Very large positions that might impact utilization rates

- Quick exits during market stress

- Exotic assets with thin Base liquidity

Base liquidity continues growing and handles most retail-sized positions without issues.

Risks and Considerations

DeFi lending on Base carries risks that users should understand before depositing funds.

Smart Contract Risk

Lending protocols rely on smart contract code that could contain vulnerabilities. While major protocols undergo extensive auditing, exploits remain possible. Mitigate this risk by:

- Diversifying across multiple protocols

- Favoring battle-tested protocols with strong audit histories

- Starting with smaller amounts before scaling up

For a comprehensive overview of DeFi lending safety, read our guide on whether DeFi lending is safe.

Bridge Risk

Moving assets to Base requires bridging, which introduces additional smart contract risk. The official Base bridge inherits Ethereum's security, while third-party bridges have their own trust assumptions.

Consider:

- Using the official bridge for larger amounts despite longer withdrawal times

- Keeping only necessary capital on Base rather than your entire portfolio

- Understanding challenge periods for withdrawals to mainnet

Liquidity Risk

Base's younger ecosystem means liquidity could dry up faster than mainnet during extreme market conditions. Withdrawal demand might spike precisely when you want to exit.

Maintain awareness of:

- Protocol TVL trends

- Utilization rates approaching 100%

- Market-wide liquidity conditions

Rate Volatility

DeFi lending rates change constantly based on supply and demand. The 4% APY you deposit at might drop to 2% or rise to 8% within weeks. Unlike traditional savings accounts, DeFi yields offer no guarantees.

Plan for rate variability when projecting returns. Historical rates provide context but do not predict future yields.

Regulatory Uncertainty

DeFi's regulatory status continues evolving. While Base benefits from Coinbase's regulatory positioning, broader DeFi regulation could impact protocol operations or user access.

FAQ

What is the minimum amount needed to lend on Base?

Base's ultra-low fees make lending viable at almost any amount. Users can profitably deposit as little as $50-100 since transaction costs remain under $0.01. However, many protocols have practical minimums around $10-50 due to dust thresholds. For meaningful yield generation, most users deposit $500 or more.

How do Base yields compare to centralized alternatives?

Base DeFi yields typically exceed centralized alternatives like exchange earn programs or traditional savings accounts. While high-yield savings accounts offer 4-5% APY, Base lending often matches or exceeds these rates with additional benefits: permissionless access, no KYC requirements, and full custody of your assets. The tradeoff involves smart contract risk and self-custody responsibility.

Can I lose money lending on Base?

Lending protocols protect depositors from borrower defaults through overcollateralization requirements. Borrowers must maintain collateral worth more than their loan. However, you can still lose funds through smart contract exploits, bridge failures, or extreme market events causing liquidation cascades. Principal protection is not guaranteed in DeFi lending, unlike FDIC-insured bank deposits.

Conclusion

Base represents a compelling destination for DeFi lending in the current market. The combination of institutional backing, low costs, and growing protocol diversity creates genuine opportunities for yield generation.

Stablecoin lenders can earn 3.5-4.5% APY on USDC through established protocols like Aave and Morpho, with transaction costs measured in fractions of a cent rather than dollars. This cost efficiency makes Base particularly attractive for smaller depositors and active position managers.

The network's connection to Coinbase provides infrastructure advantages and potentially easier onboarding for mainstream users. As the ecosystem matures, expect continued growth in liquidity depth and protocol options.

Start exploring Base lending opportunities through Superlend's discovery interface, which aggregates yields across protocols for easy comparison. Whether you are deploying stablecoins for passive income or building more complex yield strategies, Base offers the infrastructure to execute efficiently.

This content is for informational purposes only and does not constitute financial advice. DeFi lending involves risks including smart contract vulnerabilities, market volatility, and potential loss of principal. Always conduct your own research and consider your risk tolerance before participating in DeFi protocols.