USDC lending earns 3-8% APY with minimal volatility risk. Your principal stays close to $1 while you earn interest that often exceeds traditional savings accounts.

Superlend aggregates 350+ money markets across 11+ chains, making it easy to compare USDC rates across Aave, Compound, Morpho, and other protocols from one dashboard. This guide covers where to find the best rates, how to get started, risks to consider, and automated strategies through SuperFund.

What is USDC Lending?

USDC lending is the process of depositing your USDC into a DeFi protocol so that other users can borrow it. In exchange for providing this liquidity, you earn interest on your deposit.

How It Works

When you lend USDC through a protocol like Aave or Compound, your funds go into a shared liquidity pool. Borrowers can then take loans from this pool by providing collateral – typically other crypto assets worth more than what they're borrowing. This overcollateralization protects lenders: if a borrower's collateral value drops too low, the protocol automatically liquidates it to repay the loan.

The interest rate you earn comes directly from what borrowers pay. Protocols use algorithmic interest rate models that adjust rates based on supply and demand. When lots of people want to borrow USDC and fewer are lending it, rates go up. When there's more supply than demand, rates decrease.

Why Lend USDC Instead of Just Holding?

Holding USDC in your wallet earns you nothing. Meanwhile, inflation erodes its purchasing power over time. Lending puts your stablecoins to work.

Consider this: even a modest 5% APY means your $10,000 in USDC becomes $10,500 after a year – without any effort on your part and without exposure to crypto price volatility. Many DeFi protocols offer higher rates, especially during periods of high borrowing demand.

Non-Custodial: You Stay in Control

Unlike depositing money in a bank, DeFi lending is non-custodial. Your USDC goes into a smart contract – not a company's account. You maintain ownership and can withdraw at any time (subject to liquidity availability). No bank can freeze your funds or deny you access. No middleman takes a cut before passing interest to you.

This direct relationship between lenders and borrowers, mediated only by transparent code, is what makes USDC yield in DeFi fundamentally different from traditional finance.

Where to Lend USDC

The DeFi ecosystem offers multiple protocols for lending USDC, each with its own characteristics. Here are the major platforms you should know:

Aave

Aave is the largest DeFi lending protocol by total value locked. It operates across multiple chains including Ethereum, Arbitrum, Polygon, Base, and more. Aave's strength lies in its track record – it has processed billions in loans without major security incidents. The protocol offers variable interest rates that adjust in real-time based on utilization.

Compound

Compound pioneered the algorithmic money market model that most lending protocols now use. It's one of the most battle-tested protocols in DeFi. While historically focused on Ethereum mainnet, Compound has expanded to other chains. It's known for its simplicity and reliability.

Morpho

Morpho optimizes lending rates by matching lenders directly with borrowers where possible, reducing the spread between what borrowers pay and lenders earn. Morpho now offers curated vaults that provide exposure to multiple lending markets, giving users access to optimized yields without managing positions manually.

Euler

Euler offers permissionless lending markets with innovative risk management features. The protocol has seen significant growth and provides competitive rates, particularly for USDC and other stablecoins. Euler's modular design allows for customized lending pools with different risk parameters.

Fluid

Fluid combines lending with decentralized exchange functionality, creating unique capital efficiency. By using deposited assets as liquidity for both lending and trading, Fluid can offer attractive rates. It's particularly popular on newer chains where it has gained significant market share.

Rate Comparison

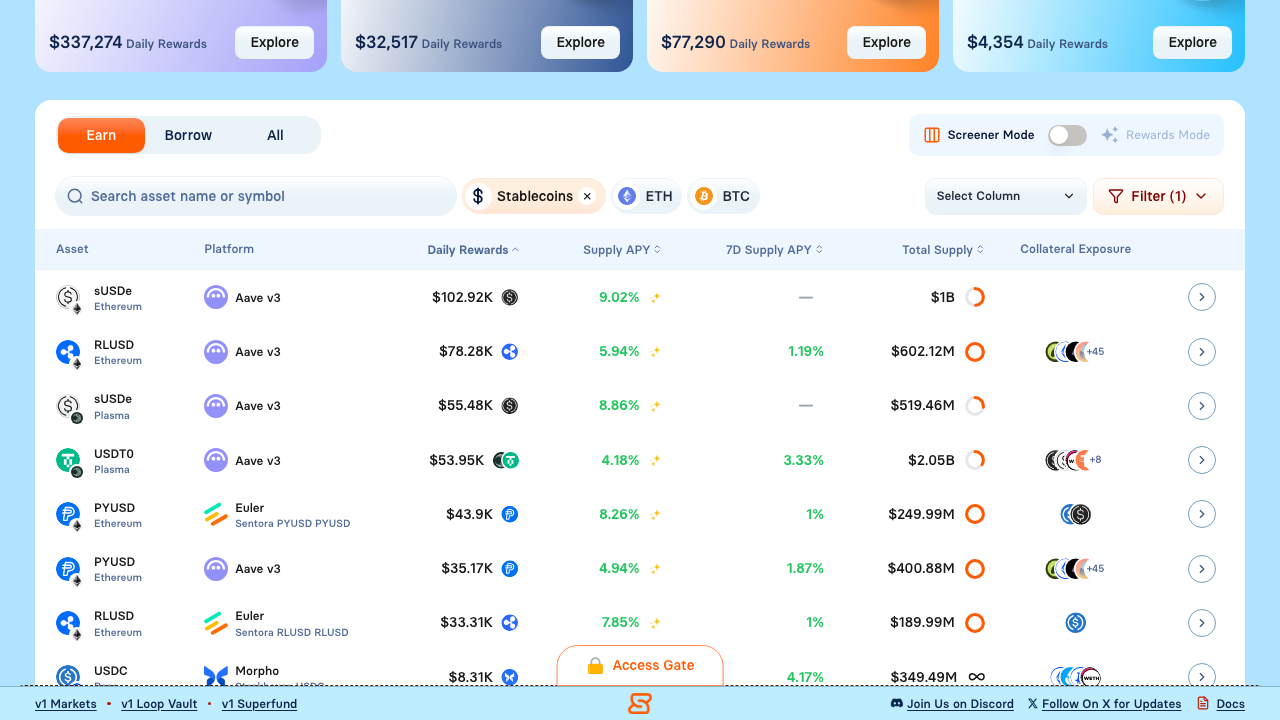

USDC lending rates vary significantly across protocols. You can compare current rates across all protocols and chains on Superlend's Discover page – filter by Stablecoins to see all options.

To compare current rates across all these protocols in real-time, use the Superlend aggregator – it pulls data from 350+ markets so you can find the best opportunity at any moment.

USDC Yields Across Chains

Where you lend matters almost as much as which protocol you use. The same protocol can offer vastly different rates on different blockchains.

Ethereum Mainnet

Ethereum remains the largest DeFi ecosystem with the deepest liquidity. USDC lending rates here tend to be moderate – not the highest, but backed by the most established markets. The main drawback is gas costs: depositing or withdrawing can cost $10-50 depending on network congestion, making it impractical for smaller positions.

Base

Base has emerged as a major DeFi destination, offering Ethereum security with dramatically lower transaction costs. Many protocols have launched on Base, and competition for users has pushed yields higher. Gas costs of just cents per transaction make Base attractive for lenders of all sizes.

Arbitrum

Arbitrum hosts a mature DeFi ecosystem with strong lending markets. As one of the first major Layer 2 networks, it has deep liquidity and multiple established protocols. Transaction costs are low, typically under $1, making it practical for active yield management.

Polygon

Polygon offers extremely low transaction costs and a wide range of DeFi protocols. While its lending markets are smaller than Ethereum mainnet, this sometimes translates to higher rates due to less competition among lenders.

Chain Comparison

Compare USDC and stablecoin rates across protocols on Superlend

Compare USDC and stablecoin rates across protocols on Superlend

The best chain for you depends on your position size. If you're lending $100,000+ in USDC, Ethereum mainnet's deep liquidity might justify the higher gas costs. For smaller amounts, Layer 2s like Base or Arbitrum make more sense.

How to Start Lending USDC

Ready to earn interest on USDC? Here's a step-by-step guide to get started.

Step 1: Choose Your Protocol and Chain

Consider these factors:

- Current APY: Higher is better, but extremely high rates may not be sustainable

- Protocol reputation: Established protocols like Aave and Compound have longer track records

- Liquidity: More liquidity means easier withdrawals when you need them

- Gas costs: Factor transaction fees into your expected returns

Step 2: Connect and Deposit

- Navigate to your chosen protocol (or use Superlend to compare and deposit across protocols)

- Click "Connect Wallet" and approve the connection

- Select USDC from the list of assets

- Enter the amount you want to deposit

- Approve the USDC spend (first-time only)

- Confirm the deposit transaction

Once your transaction confirms, you'll start earning interest immediately. Most protocols show your earnings in real-time, updating with each block.

Step 3: Monitor Your Position

While USDC lending is largely passive, you should periodically check:

- Current APY: Rates change based on market conditions

- Protocol health: Stay informed about any security issues or governance changes

- Opportunity cost: Better rates might become available elsewhere

You can view all your lending positions across protocols using the Superlend dashboard, making it easy to track performance and compare opportunities.

Step 4: Withdraw When Needed

Withdrawing is straightforward:

- Navigate to your lending position

- Click "Withdraw"

- Enter the amount (or click "Max" for everything)

- Confirm the transaction

Note: If utilization is very high (meaning most deposited funds are currently borrowed), you might not be able to withdraw your full balance instantly. This is rare for USDC on major protocols but worth understanding.

Risks of USDC Lending

No investment is without risk. Here's what you need to understand before lending your USDC.

Smart Contract Risk

Every DeFi protocol runs on smart contracts – code that executes automatically on the blockchain. If there's a bug or vulnerability in this code, funds can potentially be lost or stolen. Even audited protocols carry this risk, though established protocols with long track records and multiple audits are generally considered safer.

How to mitigate: Stick to well-established protocols with extensive audit histories. Consider diversifying across multiple protocols rather than putting all your USDC in one place.

USDC Depegging Risk

USDC is designed to maintain a $1 value, backed by cash and short-term Treasury bonds held by Circle. However, stablecoins can temporarily deviate from their peg during market stress. In March 2023, USDC briefly dropped to $0.87 due to concerns about Circle's banking partners before recovering within days.

How to mitigate: Understand that while significant depegging is rare, it's not impossible. USDC has consistently returned to peg, but keep this tail risk in mind.

Protocol Risk

Beyond smart contract bugs, protocols can face governance attacks, oracle manipulation, or economic design flaws. Newer or less-tested protocols carry higher protocol risk than established ones.

How to mitigate: Research protocols before depositing. Look at TVL trends, audit reports, team backgrounds, and how the protocol has handled any past issues. The DeFi community's collective due diligence is a valuable resource.

Liquidity Risk

If a lending pool has very high utilization – meaning almost all deposited funds are borrowed – you might not be able to withdraw immediately. You'd need to wait for borrowers to repay or for new depositors to add liquidity.

How to mitigate: Check utilization rates before depositing. Avoid pools that consistently run above 85-90% utilization if you might need quick access to your funds.

Risk Management Best Practices

- Diversify across multiple protocols and chains

- Start with smaller amounts while you learn

- Never invest more than you can afford to lose

- Stay informed about the protocols you use

- Keep some USDC liquid for unexpected needs

Automated USDC Yield with SuperFund

Manually tracking rates across dozens of protocols and chains is time-consuming. What if your USDC could automatically flow to the best opportunities?

That's exactly what SuperFund offers. SuperFund is a yield vault that automatically allocates your USDC across top lending protocols like Aave, Morpho, Euler, and Fluid – constantly optimizing for the best risk-adjusted returns.

How SuperFund Works

When you deposit USDC into SuperFund, your funds are automatically deployed across multiple vetted lending markets. The vault continuously monitors rates and rebalances to capture better yields, handling all the complexity behind the scenes.

Benefits of Automated Yield

- Set and forget: No need to manually compare rates or move funds

- Gas efficiency: The vault batches transactions, reducing the cost of rebalancing

- Diversification: Your USDC is spread across multiple protocols, reducing single-protocol risk

- Professional management: Allocation strategies are designed by DeFi experts

Getting Started with SuperFund

- Visit the Vaults section on Superlend

- Connect your wallet

- Deposit USDC

- Earn optimized yield automatically

SuperFund is ideal for users who want exposure to USDC lending yields without the overhead of actively managing positions across multiple protocols.

Frequently Asked Questions

What APY can I expect from USDC lending?

USDC lending rates typically range from 3% to 10% APY, depending on market conditions, the protocol, and the chain. During periods of high borrowing demand – such as during bull markets when traders want leverage – rates can spike higher. During quiet periods, they may settle at the lower end. Rates are variable and change constantly, so checking current rates on Superlend before depositing is always a good idea.

Is USDC lending safe?

USDC lending through established protocols has a strong track record, but it's not risk-free. The main risks are smart contract vulnerabilities, potential USDC depegging, and protocol-specific issues. Using well-audited protocols like Aave and Compound, diversifying across multiple platforms, and only lending what you can afford to lose are prudent risk management practices.

Can I withdraw my USDC anytime?

In most cases, yes. DeFi lending is designed to allow withdrawals at any time. However, if a pool has very high utilization (most funds are borrowed), you might need to wait for liquidity. This is uncommon for USDC on major protocols, which typically maintain healthy liquidity buffers.

How is lending different from staking?

Lending involves depositing your assets into a pool that borrowers can access, earning interest from borrowers' payments. Staking typically refers to locking tokens to help secure a proof-of-stake blockchain, earning rewards from the protocol itself. USDC lending earns yield from borrower interest, not from blockchain validation rewards.

Conclusion: Start Earning Yield on Your USDC

USDC lending offers a compelling opportunity: earn passive yield on a stable asset without the volatility of typical crypto investments. With established protocols, multiple chains to choose from, and aggregators like Superlend to find the best rates, getting started has never been easier.

Whether you prefer hands-on management – comparing rates and moving funds between protocols – or automated optimization through SuperFund, there's an approach that fits your style.

Ready to put your USDC to work?

- Compare rates across 350+ markets: app.superlend.xyz

- Automate your USDC yield: Vaults section on Superlend

- Learn more about DeFi lending: Complete Guide to DeFi Lending

- Explore stablecoin strategies: Stablecoin Yield Strategies

- Understand DeFi safety: Is DeFi Lending Safe

This article is for educational purposes only and does not constitute financial advice. DeFi involves risks including smart contract vulnerabilities and potential asset depegging. Rates are variable and past performance does not guarantee future results. Always conduct your own research before making investment decisions.