Ethereum holders face a common dilemma: you believe in ETH's long-term potential, but watching it sit idle in your wallet feels like a missed opportunity. Selling isn't an option – you want to maintain your exposure. So what can you do?

The answer lies in ETH lending rates. By supplying your Ethereum to DeFi lending protocols, you can earn passive income while keeping full ownership of your assets. When you're ready to exit, you simply withdraw your ETH plus the interest you've earned.

ETH lending rates currently range from 1.5% to 4% APY on base lending, but you can reach 4-8% by stacking yields with liquid staking tokens. This guide covers current rates across major protocols, the LST yield stacking strategy, and the risks involved.

How ETH Lending Works

ETH lending works like this: you supply Ethereum to a lending protocol, and borrowers pay interest to use it. Here's the step-by-step process:

1. Supply ETH to a Protocol

When you deposit ETH into a lending protocol like Aave or Compound, your funds enter a shared liquidity pool. In return, you receive a token representing your deposit – for example, aETH on Aave or cETH on Compound. This token tracks your principal plus accrued interest.

2. Earn From Borrowers

Other users borrow from the pool by putting up collateral – typically other crypto assets worth more than what they're borrowing. The interest they pay gets distributed to all lenders in the pool, proportional to their share.

3. Keep Your ETH Exposure

Unlike selling your ETH, lending it means you maintain price exposure. If ETH goes from $3,000 to $4,000 while you're lending, you benefit from that appreciation plus the interest you've earned. Your position stays denominated in ETH.

4. Withdraw Anytime

Most lending protocols allow instant withdrawals, provided there's available liquidity in the pool. You simply swap your deposit token back for ETH and receive your original amount plus accrued interest.

The system is permissionless and non-custodial. There's no application process, no credit check, and no one else controls your funds – you can withdraw at any time through the smart contract.

Current ETH Lending Rates

Native ETH lending rates typically range from 1.5% to 4% APY, depending on market conditions and protocol. These rates fluctuate based on borrowing demand – when more people want to borrow ETH, rates increase.

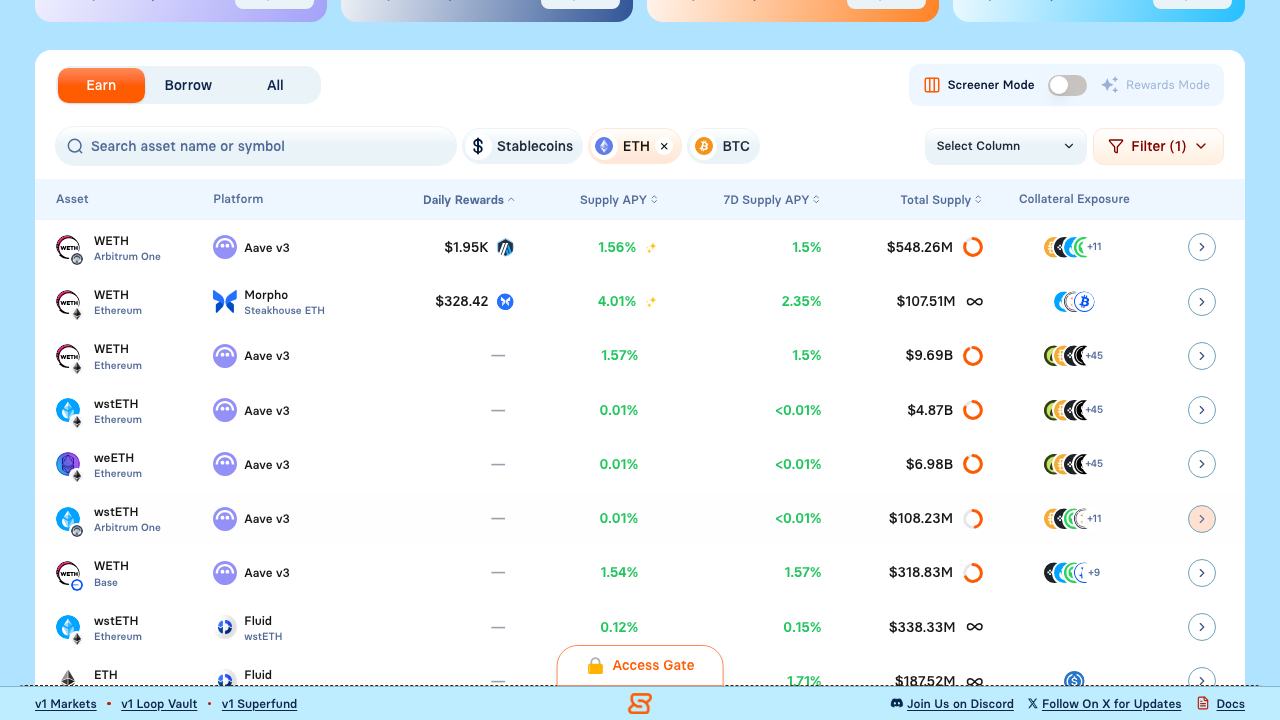

ETH Lending Rate Comparison

Compare ETH lending rates across protocols on Superlend

Compare ETH lending rates across protocols on Superlend

Rates are variable and change frequently based on market conditions. For a deeper understanding of how these protocols differ, see our Aave vs Compound comparison.

What Affects ETH Lending Rates?

Several factors influence how much you can earn lending ETH:

Borrowing Demand: When traders want to short ETH or need it for leveraged strategies, they borrow from lending pools. High demand pushes rates up.

Market Volatility: During volatile periods, borrowing activity often increases as traders adjust positions. This can temporarily spike rates.

Utilization Rate: Each pool has a utilization rate – the percentage of supplied funds currently borrowed. Higher utilization means higher rates, but also higher risk of withdrawal delays.

Alternative Yields: If staking yields are attractive, fewer people borrow ETH, keeping lending rates relatively low. When staking returns compress, lending can become more competitive.

The honest truth is that native ETH lending rates are modest. For higher yields, you need to look at liquid staking tokens.

Liquid Staking + Lending: Stacking Your Yields

Here's where things get interesting. Instead of lending native ETH, you can stake your ETH first, receive a liquid staking token (LST), and then lend that token. This stacks two yield sources together.

How It Works

- Stake ETH: Deposit ETH with a liquid staking provider like Lido (stETH), Rocket Pool (rETH), or Coinbase (cbETH)

- Earn Staking Rewards: Your LST accrues staking yield – typically 3-4% APY

- Lend the LST: Supply your stETH, rETH, or cbETH to a lending protocol

- Earn Lending Yield: Collect an additional 1-4% from borrowers

Combined Yield Comparison

The combined yield from staking plus lending varies by protocol and LST. Typical combined APYs range from 3.3% to 6.2% depending on market conditions. Check live rates on Superlend to find current opportunities.

Why LST Lending Rates Are Lower

You might notice that lending yields on LSTs are lower than on native ETH. This is intentional – borrowing LSTs is less attractive because borrowers are already paying the staking yield embedded in the token. The total yield to lenders comes primarily from staking, with lending adding a smaller boost.

Choosing Your LST

Different liquid staking tokens have different characteristics:

stETH (Lido): The most liquid and widely accepted LST. Highest borrowing demand means slightly better lending rates.

rETH (Rocket Pool): More decentralized than stETH. Slightly lower staking yield but strong community backing.

cbETH (Coinbase): Centralized but convenient for users already in the Coinbase ecosystem. Often has lower lending demand.

wstETH (Wrapped stETH): A wrapped version of stETH that doesn't rebase, making it more compatible with DeFi protocols.

For most users, stETH or wstETH offers the best balance of yield, liquidity, and protocol support.

Best Protocols for ETH Lending

Not all lending protocols are created equal. Here's how to choose based on your priorities:

Aave

Best for: Maximum security and liquidity

Aave is the largest lending protocol by total value locked, with years of battle-tested operation. Its ETH and stETH markets have deep liquidity, meaning you can deposit and withdraw large amounts without issue. Rates are typically middle-of-the-pack, but the security and reliability are unmatched.

Use Aave when you prioritize safety over maximizing every basis point of yield.

Compound

Best for: Conservative lenders who want simplicity

Compound pioneered DeFi lending and remains one of the most trusted protocols. It's straightforward to use and highly reliable. Rates tend to be slightly lower than competitors, but the protocol's conservative risk parameters provide peace of mind.

Use Compound when you're new to DeFi lending or prefer a no-frills experience.

Morpho

Best for: Yield optimization with acceptable risk

Morpho sits on top of Aave and Compound, using peer-to-peer matching to improve rates for both lenders and borrowers. When a match occurs, you get better rates than the underlying pool. When no match exists, you fall back to the base protocol.

Use Morpho when you want potentially higher yields while still benefiting from the security of established protocols.

Fluid

Best for: Users comfortable with newer protocols seeking higher yields

Fluid offers dynamic rates that can exceed competitors, particularly for LSTs. The protocol is newer but has undergone audits and is growing rapidly. Higher rates come with the trade-off of less time-tested code.

Use Fluid when you're comfortable with slightly more risk in exchange for better yields.

Risks of ETH Lending

No yield comes without risk. Before you lend your ETH, understand what you're exposing yourself to:

Price Volatility

While you maintain ETH exposure when lending, that exposure works both ways. If ETH drops 30% while you're lending, your position loses 30% in dollar terms – the 2-4% yield won't come close to offsetting that. Only lend ETH you're comfortable holding long-term.

Smart Contract Risk

Lending protocols are governed by smart contracts – code that executes automatically on the blockchain. Despite audits and battle-testing, vulnerabilities can exist. Major protocols like Aave and Compound have strong track records, but the risk is never zero.

To mitigate this:

- Stick to established protocols with high TVL

- Diversify across multiple protocols if you're lending significant amounts

- Monitor protocol news and governance

LST-Specific Risks

If you're using the LST stacking strategy, additional risks apply:

Depeg Risk: LSTs should trade close to ETH's value, but during market stress, they can temporarily depeg. In extreme cases, you might not be able to exit at a 1:1 ratio.

Slashing Risk: Validators securing the staked ETH could be penalized for misbehavior, reducing the value of the LST. Major providers like Lido have insurance mechanisms, but the risk exists.

Compounded Protocol Risk: You're now exposed to smart contract risk on both the staking protocol and the lending protocol.

Liquidity Risk

If utilization in a lending pool reaches very high levels (90%+), you might face delays withdrawing. This is rare for major assets like ETH but worth monitoring, especially for LSTs with lower liquidity.

Getting Started with Superlend

Ready to put your ETH to work? Superlend makes it easy to find the best rates across 350+ money markets:

Step 1: Visit app.superlend.xyz and connect your wallet

Step 2: Use the "Lend" tab to see current ETH and LST rates across all supported protocols

Step 3: Compare rates, utilization, and protocol details in one dashboard

Step 4: Select your preferred market and supply your assets directly through Superlend

Instead of checking Aave, Compound, and Morpho separately, Superlend aggregates everything in one place. You can see real-time rates, historical trends, and execute transactions without visiting multiple interfaces.

For deeper learning, check out our Complete Guide to DeFi Lending, explore USDC lending opportunities, or learn about understanding lending protocols.

FAQ

What's the difference between lending ETH and staking ETH?

Staking ETH involves locking it to help secure the Ethereum network, earning rewards directly from the protocol (currently ~3-4% APY). Lending ETH involves supplying it to a DeFi protocol where borrowers pay you interest (typically 1.5-4% APY). You can do both by staking first to get an LST, then lending the LST.

Can I lose my ETH by lending it?

While lending is generally safe on established protocols, risks exist. Smart contract vulnerabilities, extreme market conditions, or protocol insolvency could result in losses. Your principal remains denominated in ETH, so you're also exposed to ETH price movements.

How often do ETH lending rates change?

Rates adjust continuously based on supply and demand. They can change by small amounts every block (roughly every 12 seconds). Major rate shifts typically happen during periods of high market volatility or significant changes in borrowing demand.

This article is for educational purposes only and does not constitute financial advice. DeFi involves risks including smart contract vulnerabilities and market volatility. Rates are variable and subject to change. Past performance does not guarantee future results. Always conduct your own research before making investment decisions.